Gorodnichenko, in Yahoo Finance:

Moscow’s economy is heavily dependent on petrodollars, or dollars earned through oil and gas trading, Gorodnichenko said. Yet with Russian energy flows disrupted by sanctions, it’s unclear whether sales to friendly countries will be enough to support the Kremlin’s hefty war budget — or whether Russia will have enough access to dollars to easily import all the goods and resources its economy needs to function, he said.

This could put the Russian economy on a fast track to recession within the next 12 months, Gorodnichenko predicts.

“If they have to finance the war and they don’t have those resources, it’s not clear where they’re going to get that money,” he added. “I predict they’re going to be in for a very serious recession.”

BOFIT Notes that sanctions have been tightened on oil exports, while new EU sanctions on natural gas have been implemented.

The IMF July WEO 2019 Edition Update (released today, but based on exchange rates from April 22 to May 20) indicates that while there has been no downward revision to 2024 year-on-year growth, 2025 growth has been reduced by 0.3 percentage points to 1.5% year-on-year (The World Bank forecasts 1.4% growth for June) And this is despite the rise in oil prices. If, on the contrary, oil prices fall, we can expect, under certain conditions, a slowdown in growth.

BOFIT’s latest assessment of economic challenges was July the 5th.

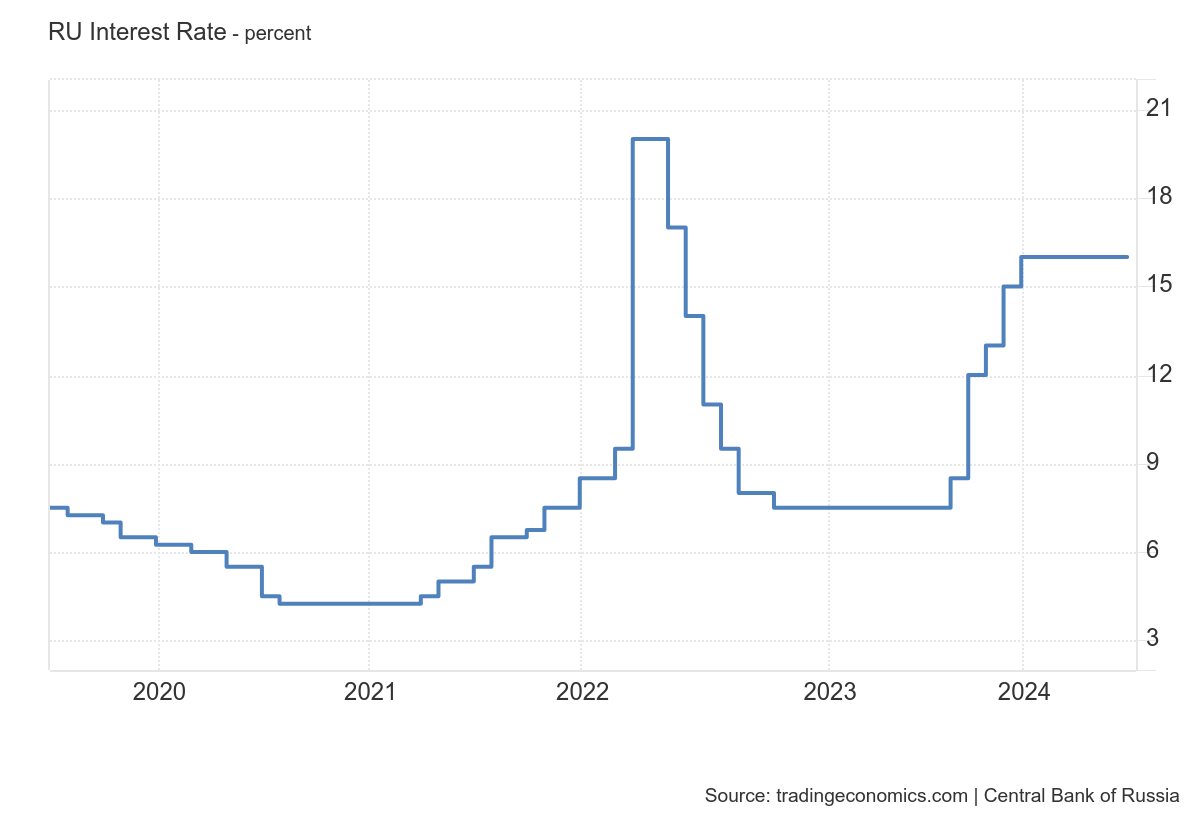

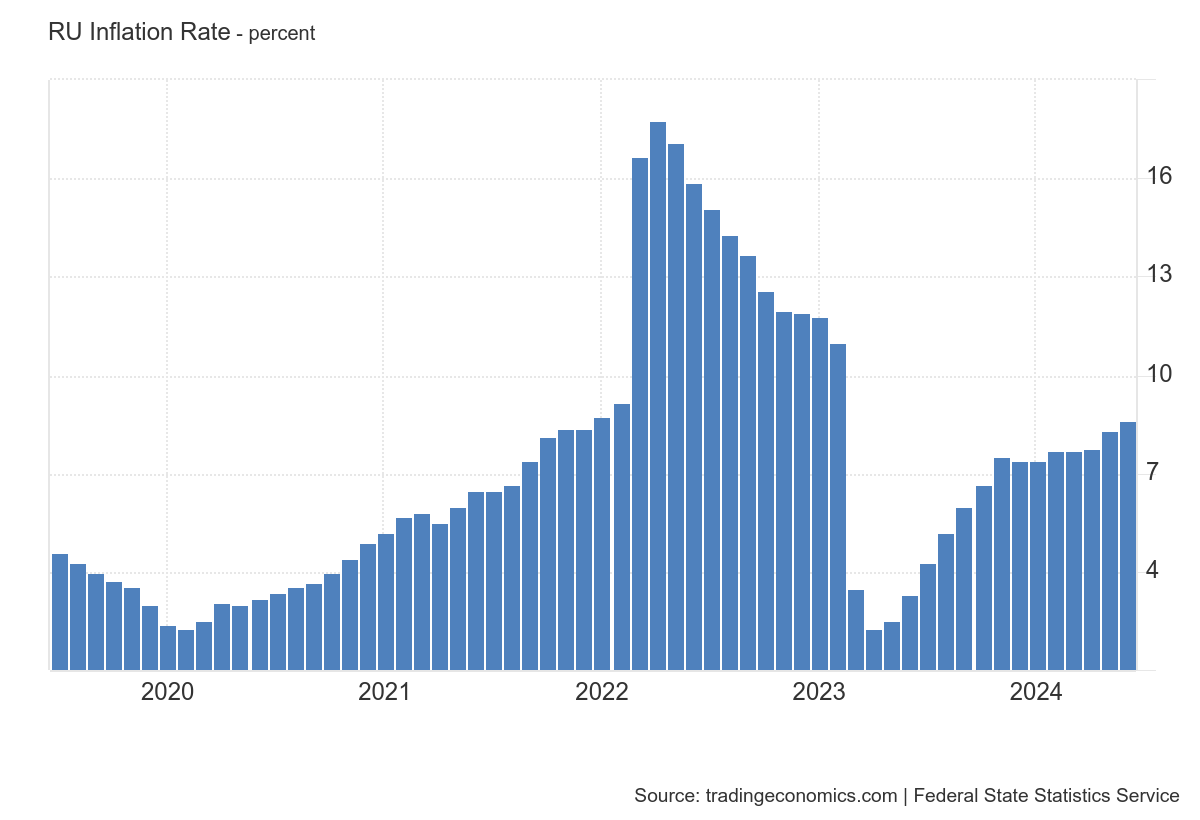

Here are some pictures of the latest monetary conditions. Note that the key rate remains high at 16%.

We do not know what the real policy rate is ex ante in the absence of a good estimate of expected inflation. Assuming adaptive expectations (lagged inflation from one year to the next is a proxy for current expected inflation), the real policy rate is positive.

With inflation at 8.6% in June, the real policy rate is 7.4%. A high real rate stabilizes the currency and tends to suppress inflation, but at the cost of a decline in economic activity in interest-rate-sensitive sectors.

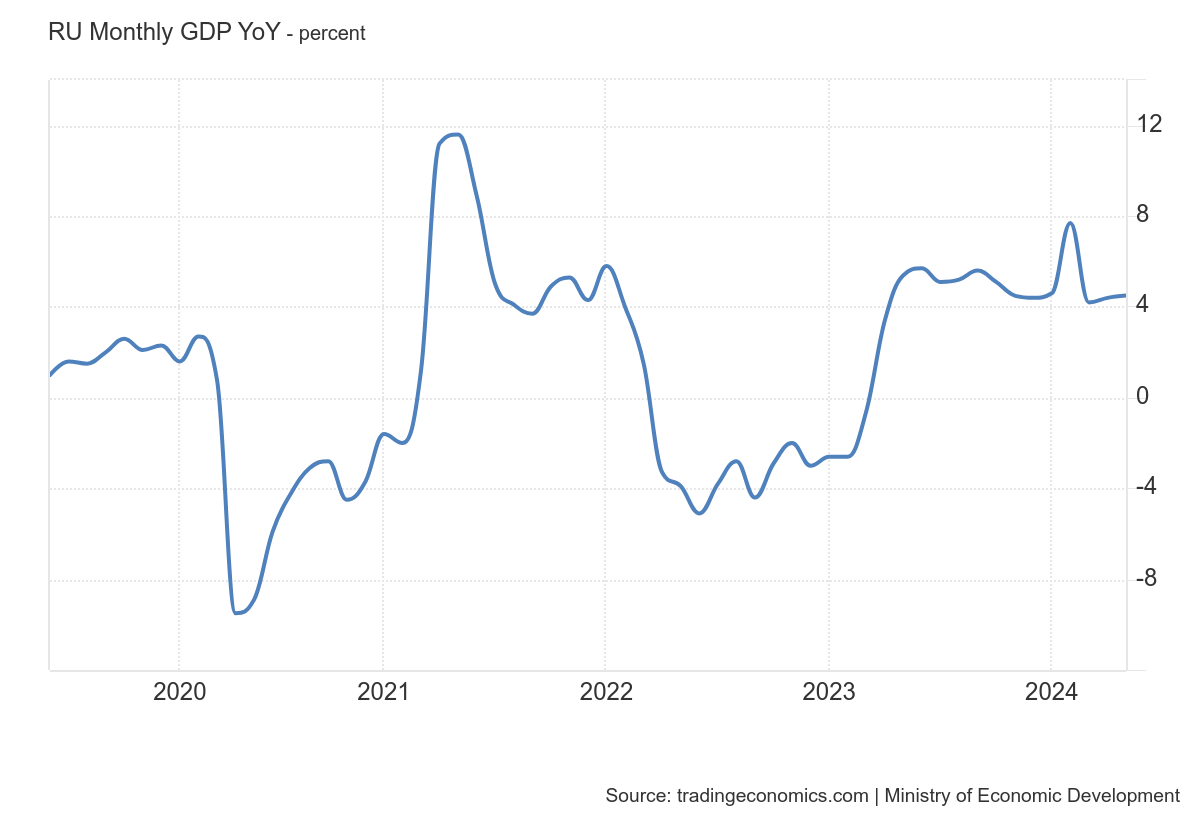

Although the forecast GDP growth (year-on-year, through May) is positive, around 4%, if we exclude defense and security spending, growth would probably be significantly lower. I haven’t done this calculation for 2023 or 2024, but hereThis is the calculation based on estimates and forecasts for 2023.