")

JHVEPhoto

Marvell Technology (NASDAQ:MRVL) is a key provider of semiconductor solutions for data center infrastructure, serving the data center core and network edge. Marvell’s data center business accounted for more than 70% of total revenue in the most recent period. quarter. Marvell expects its AI revenue from optics and custom ASICs to reach more than $1.5 billion by FY25. Additionally, the company is well positioned to grow its core switching portfolio data (active electrical cables) in the near future. I’m initiating a “Buy” rating with a one-year price target of $80 per share.

Growth in AI Optics and Custom Silicon

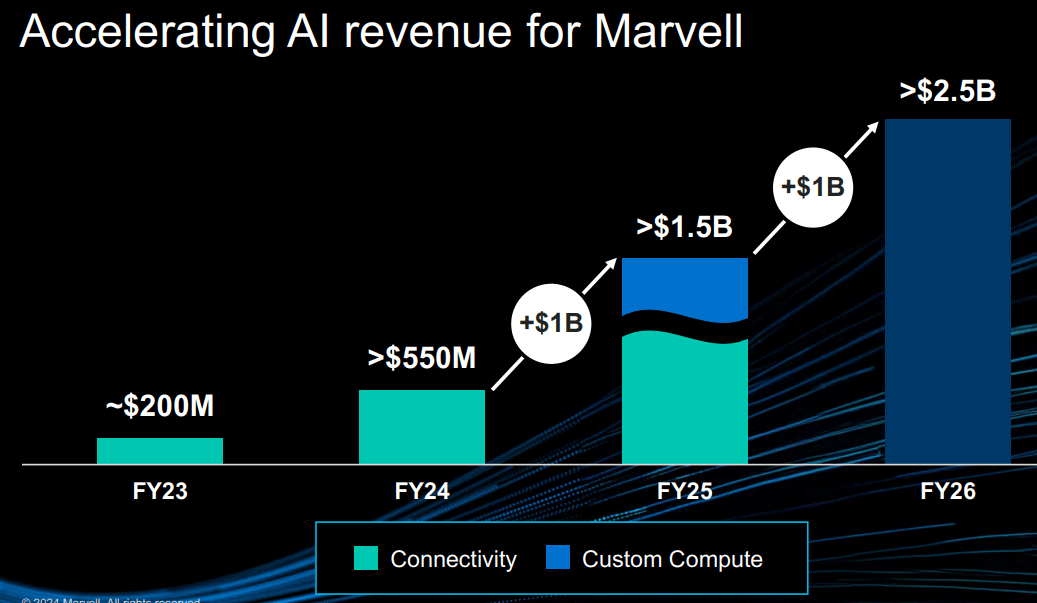

Marvell’s exposure to AI lies in its data center optics and custom silicon (“ASIC”) business. As shown in the chart below, the company is expected to generate over 1.5 billion in revenue from AI by FY25.

Marvell Investor Presentation

- AI Optics: Marvell’s optics portfolio includes pulse amplitude modulation, digital signal processors, laser drivers, trans-impedance amplifiers and data center interconnect solutions. Data centers require interconnect solutions to connect massive GPUs, routers, and switches. Marvell is well positioned to capture the rapid growth of the data center interconnectivity market.

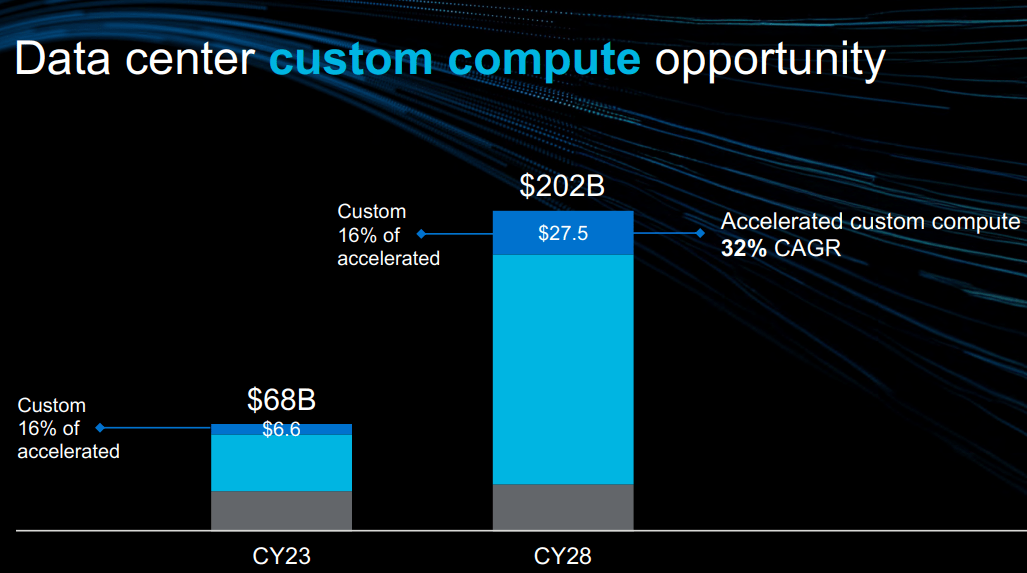

- Custom ASIC: The company develops system-on-chip solutions tailored to individual customers. For example, hyperscalers, such as Microsoft (MSFT), Amazon (AMZN) and the alphabet (GOOGLE), you can either purchase standard GPU products from Nvidia (NVDA), AMD (AMD), or Intel (INTC), or design their own chips with Marvell’s ASIC technology. According to management, Marvell worked with all the hyperscalers to design their own chips. As reported Business Insider, Marvell has approximately 15% market share in the custom ASIC market. Marvell collaborated on the production of Amazon’s 5nm Tranium chip and Google’s 5nm Axion ARM CPU chip. Additionally, Marvell has advanced its 3nm technology with these hyperscalers. As shown in the slide below, the total addressable market for custom ASICs is expected to grow at a CAGR of 32% between FY23 and FY28, driven primarily by rapid growth in AI and data centers.

Marvell Investor Presentation

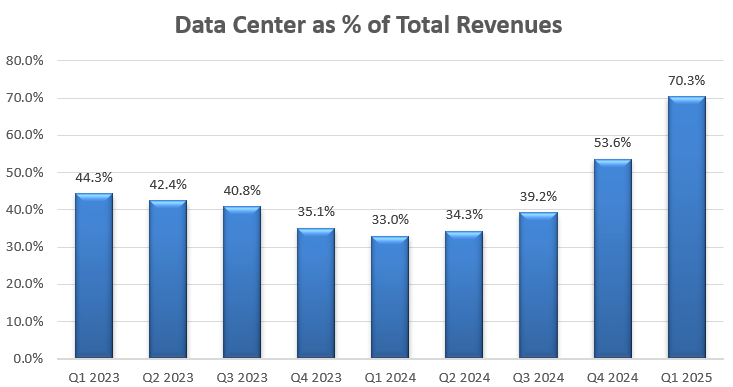

With AI currently experiencing rapid growth, I expect Marvell’s custom optics and ASIC businesses to see rapid growth in the coming years. As the chart below shows, Marvell has significantly grown its data center business in recent quarters, contributing more than 70% of total revenue for the year. Q1 FY25.

Marvell Quarterly Profit

Weakness of other cyclical activities

Marvell has 30% of its revenue in certain cyclical businesses, including enterprise networks, carrier infrastructure, consumer electronics and automotive markets. In Q1FY25, enterprise network revenue declined 58% YoY, carrier infrastructure declined 75%, consumer declined 70%, and automotive/industrial markets declined 75%. of 13% of income.

In a macroeconomic environment of high interest rates, businesses and telecommunications companies are tightening their IT budgets. Additionally, CIOs must prioritize AI spending within their limited IT budgets. These macroeconomic headwinds are causing a temporary slowdown in the business, telecommunications, automobile, and industrial markets.

Long term, I continue to expect growth in these cyclical businesses, albeit at a slower pace than data centers. In October 2022, Marvell announcement its 100G/lane active electrical (“AEC”) cables, enabling 400G, 800G and 1.6T server-to-switch and switch-to-switch solutions. Marvell’s Ethernet controllers and network adapters could continue to grow alongside the enterprise Ethernet market. That said, these cyclical activities will likely continue to cause headwinds in the near term.

Recent result and outlook for FY25

Marvel released its Q1 FY25 results on May 30, reporting a 12.2% decline in revenue and a 21.8% decline in net profit, primarily driven by notable declines in 5G, automotive/industrial, enterprise networking and operators, as indicated previously.

My biggest takeaway from the quarter is the strong growth in data center activity, which increased 87% year-over-year and 7% sequentially. During the call for results, management expressed optimism about the growing demand for AI applications. The company has started the initial ramp of custom AI computing silicon with hyperscalers. I expect revenue contribution from custom ASICs to begin in FY25.

For the second quarter, the company expects sequential revenue growth of 8%, primarily driven by strong data center growth.

Marvell Investor Presentation

I am considering the following factors for FY25:

- Data Center: Given Marvell’s strong growth in Q1, I expect data center activity to grow 70% in FY25, driven by both interconnectivity and ASIC activities personalized. It’s worth noting that Marvell only generated $2.2 billion in data center revenue in FY24; therefore, they have a small base to grow rapidly for their interconnectivity and custom ASIC businesses.

- Enterprise Networks and Carrier Infrastructure: End markets are currently experiencing inventory destocking, and it is possible that the market will begin to normalize and recover in the second half of FY25. To be cautious, I expect Marvell’s revenue to decline 40% in FY25.

- The automotive semiconductor market is normalizing in the post-pandemic period. Global S&P forecasts that global sales of new light vehicles in 2024 will see a year-over-year increase of 2.8%. Automotive is only a small part of Marvell’s business, accounting for less than 7% of total revenue. I expect its revenue to grow 3% in FY25.

Putting this together, I expect Marvell to grow revenue by 7.3% in FY25.

Assessment

To estimate normalized revenue growth beyond FY25, I consider the following:

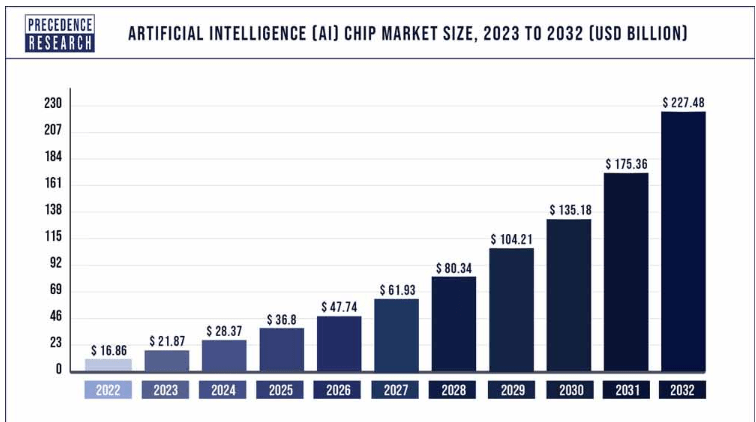

- Data Center: I’m bullish on Marvell’s custom silicon and AI optics businesses. Priority search predicted This AI chip market will grow by 29.72% between 2023 and 2032. Given the rapid adoption of AI by enterprise customers and hyperscalers, I expect Marvell’s data center to see a growth of more than 30% beyond FY25.

Priority search

- Enterprise networks and 5G: The market has grown in the mid-single digits in the past. Enterprise customers must invest in edge networks in the future to deploy AI training and inference workloads. I expect Marvell to grow its business 5% per year.

- Automotive chips: According to several automotive chip companies, such as ON Semiconductor (ON) and NXP Semiconductors (NXPI), the automotive semiconductor market is expected to grow at over 12% in the future. As such, I assume Marvell will be able to grow alongside market growth in the near future.

As such, I assume Marvell will grow revenue by 16% annually beyond FY25.

In April 2021, Marvell completed the acquisition from Inphi for $10 billion, a leading high-speed data interconnection platform for the data center market. Looking back, this was a tremendous acquisition that contributed significantly to Marvell’s current technological advancements in the data center market.

Additionally, Marvell acquired Innovium in August 2021 to accelerate its networking solutions for cloud and edge data centers. These acquisitions have resulted in enormous depreciation costs for Marvell in recent years, amounting to more than $1 billion in annual depreciation. In FY23, Marvell still had $4 billion of intangible assets on its balance sheet, and I calculate that its acquisition amortization costs will begin to gradually decline in the near future, contributing to opportunities for expansion of company margins.

I estimate that Marvell will increase its operating expenses by 13.5% per year, resulting in an increase in its annual margin of 360 basis points.

Additionally, I assume the company will spend 10% of its total revenue on M&A, contributing to 3.3% revenue growth. The summary of the DCF model is as follows:

Marvell DCF – Author’s calculations

I calculate free cash flow from equity as follows:

Marvell FCFE – Author’s calculations

The cost of equity is calculated at 17% assuming: a risk-free rate of 4.2%; beta 1.88; equity risk premium 7%. Discounting all future FCFE, the one-year price target is calculated at $80 per share.

Main risks

Cyclical Companies: Marvell is a semiconductor company that operates in a highly cyclical industry. In the short term, its 5G, enterprise networks, automotive and industrial businesses are in a down cycle. Long term, I expect Marvell’s revenue growth to remain volatile and investors should prepare for this volatility each quarter.

Exposure to China: China accounts for 43% of total revenue and Marvell is exposed to risk from any potential regulatory activity such as tariffs, export controls and sanctions. The outcome of the US presidential election could also impact Marvell’s exposure to export restrictions.

Increasing stock-based compensation: Marvell spent 11.1% of its total revenue on stock-based compensation (“SBC”) in FY24, an acceleration from 9.3% in FY23. As a semiconductor company, Marvell’s SBC expenses are quite high. Management must now properly manage their expenses in SBC.

Conclusion

I like Marvell’s leadership position in the AI optics and custom ASIC markets, and their business is very relevant, especially with the growing demand for data centers and AI computing. I’m initiating a “Buy” rating with a one-year price target of $80 per share.