")

Jean Touscany

When the market offers to teach you a lesson, it’s usually a good idea to pay attention. I have long been quite positive about the quality of Kirby(NYSE:KEX) management and business, especially with the strong presence of the company share of the U.S. inland tank barge market and emphasis on disciplined fleet management. I was also positive about overall industry dynamics as supply and demand shifted in Kirby’s favor given the expansion of Gulf Coast petrochemical production and limited fleet growth industrial.

Here’s where I messed up – in my last article about the company I have been overly preoccupied by concerns about the impact of a weakening U.S. economy on demand for petrochemicals (as well as demand for products and services provided by Kirby’s Distribution and Services segment) and by the how the street could take a more cautious view of economically sensitive issues. carriers like Kirby. I decided that some underpricing wasn’t enough and wanted to wait for an even better entry price.

It was absolutely not the right decision. Stocks then fell a few points, but only briefly, as the barge market continued to tighten, propelling prices to a multi-decade high and setting the stage for years of strong margins. With this, the shares are up over 60% and this falls into the category of “missed opportunities”. I don’t think Kirby’s potential has plateaued and there are still reasons to consider this game well done in a tightening market.

A fairly classic supply-demand imbalance

The inland tank barge market has experienced many cyclicalities over the years, some driven by economic cycles and some (arguably more) by the expansion and contraction of operators’ fleets. With COVID-19 putting many operators under strain and with rather minimal newbuild activity since then (less than 1% of the fleet in any given year), as well as scrap rates higher than new constructions and new maintenance regulations, there is now a shortage of barges compared to growth. demand driven by increasing refining/petrochemical production capacity in the Gulf Coast region.

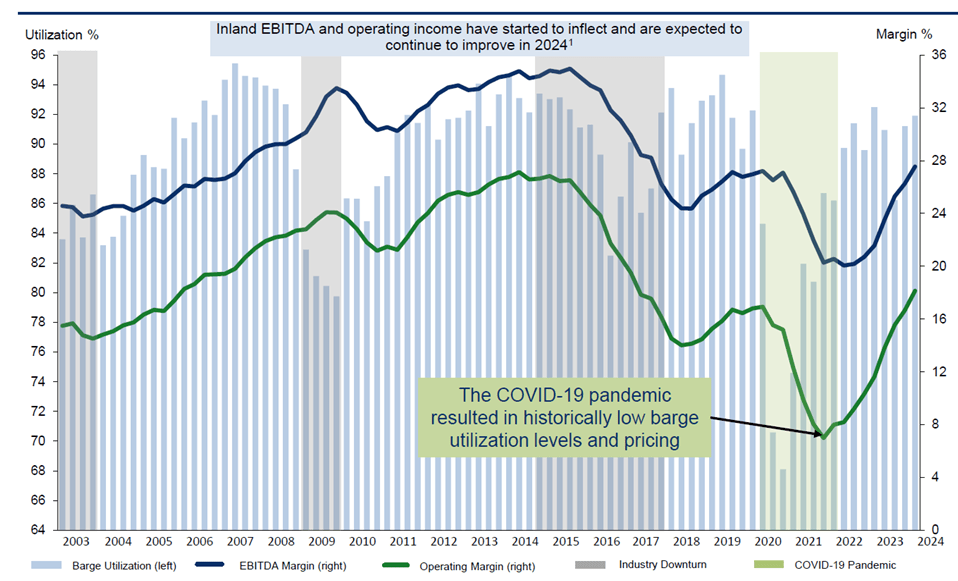

The following chart, from Kirby’s current investor presentation, highlights some of the historical cyclicality and its impact on utilization and margins:

The cyclicality of barge activity (Kirby Investor Presentation)

Domestic spot rates are now between $9,500 and $10,000 (up from $9,000 a year ago) and Kirby’s most recent domestic revenue per ton-mile ($0.117) was, I believe, the highest the company has achieved in over two decades or more. Thanks to strong pricing, healthy utilization and disciplined cost management, Kirby is seeing margin improvement of more than 300 basis points year-over-year in its domestic business and this momentum could continue until 2027 taking into account delivery times for new constructions.

Speaking of new builds, there isn’t as much shipyard capacity as there used to be and between limited capacity and inflation, the cost of a newly built inland tank barge has roughly doubled from shipyard levels. before the pandemic (to reach around $4 million). At this price, it takes day rates of around $14,000 to generate a double-digit IRR, although I will note that carriers have accepted lower IRRs in previous cycles. So I expect new construction activity to pick up before rates hit that $14,000 per day level.

For now, however, Kirby is doing quite well with about 30% share of the inland barge market and little new competition in sight, as well as good demand prospects from Gulf Coast producers (subject of a certain economic sensitivity). I would also like to note that Kirby is one of the only ways to play this dynamic – MPLX (MPLX) certainly has a large fleet of barges, but also a more diversified set of intermediate energy assets.

The coastline is experiencing a similar attractive dynamic

Although Kirby’s inland tank barge business is the main driver here, the coastal business has also come to life here recently. Operating conditions have been tougher here for a while, but Kirby has stayed the course and pulled out of some less promising parts of the business and now stands as a leaner operator (#2 in capacity total) serving blue-chip oil and petrochemical clients.

Much like the inland barge market, the economics of new construction of coastal barges argue for higher prices if new capacity is to come to market (new construction costs increased from $85 million before the pandemic to 130 million dollars).

In the most recent quarter, Kirby reported strong mid/high utilization of 90% and contract renewal prices increased 20% year-over-year, while spot prices increased by 30 %. This led to the best margin for the company in almost a decade, ranging from “high single digits to low double digits” (unfortunately, Kirby does not release specific profits/margins for Inland and coastal areas).

The economics of inland barges depend in part on the cost advantages of barges over rail or road transport, and the same is true for coastal transport. In both cases, these companies benefit not only from the increased demand for inputs and petrochemicals, but also from the reluctance to approve and build new pipelines, with barges used to transport crude to refineries and then to transport refined products to markets along inland waterways and the coast.

Energize D&S

Kirby’s Distribution and Services business has always been an odd duck, with lower margins and less consistent performance than the barge operations. While there have long been debates about whether Kirby should continue these operations, they are here for the foreseeable future and worth discussing.

The first quarter of this year saw a revenue decline of almost 2% year-on-year, largely due to weaker demand in the oil/gas segment (down 43%), the number of rigs drilling in the United States declining at a double-digit rate. The commercial/industrial sector declined by 7%, as increased maritime activity was offset by lower demand on the roads.

The most notable activity was the power generation business (up 50%), which has now grown to such an extent that the company divides it into separate reports and discussions. This company provides backup power systems to a wide range of customers, including industrial, retail and data center sites, and does so as a distributor, manufacturer and service provider for system manufacturers such as caterpillar (CAT). Management believes this business could generate a double-digit margin at scale (compared to an overall D&S margin of 6.6% in the quarter), and with increased interest in microgrids, not to mention growth in data center construction, I could see this segment providing interesting growth for years to come.

Perspectives

While the U.S. economy still appears sluggish in some respects, I’m not going to dwell on the misconception that the market will avoid these stocks out of fear that a slowdown in activity will put enough pressure on petrochemical demand. to impact petrochemical demand. Kirby in a meaningful way. Instead, I expect the company to benefit from good leverage through 2026/2027 thanks to inland and coastal barge fundamentals that argue for strong pricing and expansion of the margin of the upward cycle.

To be clear, I’m not saying there isn’t economic risk here, but I think the risk is more than offset by the dynamics of the barge sector. Rather, the biggest threat to Kirby from quarter to quarter will likely be river operating conditions, with poor weather, lockage delays and other navigational hazards posing a risk to revenue generation.

Kirby did about what I expected in FY23 (revenue of $3.09 billion vs. my estimate of $3.08 billion and EBITDA of $557 million vs. my estimate of $565 million) and the first quarter results give me no reason to change my numbers for FY24. I’m looking for ~7% year-over-year revenue growth this year, with ~250 basis points year-over-year increase in EBTIDA margin and better free cash flow generation.

I expect revenue growth of around 6% between 2023 and 2027 (roughly double the long-term growth rate), with EBITDA margins heading towards the mid-20% and margin of free cash flow peaking in the mid to high range. teenagers. I’m not too concerned about Kirby embarking on an aggressive new build program; historically, they preferred to acquire younger barges to renew their fleet.

Kirby doesn’t look that cheap in terms of discounted cash flow, but that’s to be expected when the company enters its margin expansion phase. A forward EBITDA multiple of 12.5x (a fair value of $129) can be supported by short-term margins/returns (ROIC, et al), and it is not that uncommon for the stock to trade up in bull cycles, so if you If I want to argue that Street will happily pay 15x EBITDA for impending earnings momentum, I don’t really disagree. Likewise, you can look at what the market has paid in terms of P/E during past bull cycles and make a case for a fair value in the $130 range.

The essential

Taking a neutral stance on Kirby in October of last year and being more positive today is less about chasing the stock and more about realizing I was too focused on short-term sentiment risk and that I became stingy hoping for an even more attractive entry point. I thought the shares were undervalued then, and I still see an argument for a higher price based on strong pricing and growing margins.

At today’s senior level, it’s a difficult decision for a variety of reasons. I can make the case that Kirby is trading at $150 or more based on valuations from past cycles and the potential for higher, bullish quarters, but is that enough to take the risk on what has always been a stock cyclical?

I’m not ready to say today that the cycle has gone as far as it can go or that the market has fully priced in the potential of this current supply/demand imbalance and margin expansion opportunity, but I still advises a little caution. and I certainly wouldn’t consider this a buy-and-hold idea for long-term investors.