")

Agence_South

Investment thesis

I had it before Keysight cutlery (NYSE:KEYS) where I talked in more depth about the business model and the implicit quality I think it possesses. In this article I decided that the best thing was to hold on for the moment and since then, the company has fallen 11% compared to the S&P500’s 2% appreciation.

While this may not seem like a significant drop, the current 33% drop from the last peak is one of the largest in Keysight’s history, and the drop has only been larger three times. Considering this and adding that on May 20 the company presented Second quarter 2024 resultsI would like to delve deeper into what has changed in the company since then.

Key draw (Koyfin)

Q2 2024

The results summary indicates that the company slightly exceeded expectations, but given that we are currently in a very negative economic environment for the company, it is worth noting that exceeding the forecasts provided by management itself a quarter ago.

Given the base orders of $1.14 billion in the first quarter, we expect second quarter revenue to be between $1.190 billion and $1.210 billion and second quarter earnings per share to be between 1 .34 and $1.40.

Neil Dougherty, CFO, during Call for first quarter 2024 results

The not-so-positive aspect that caused the market to be so cautious with Keysight is that during the second quarter of 2024, revenues declined by 12.5% (even considering that expectations were exceeded) and forecasts Initial estimates for the third quarter would imply a decrease of almost 14%, so it should surprise no one if this fiscal year ends with a double-digit sales decline.

| Estimate | Real | Beat/Miss | |

| Income | $1.20 billion | $1.22 billion | 1.0% |

|---|---|---|---|

| EBITDA | $327 million | $332 million | 1.4% |

| PES | $1.39 | $1.41 | 1.6% |

Author’s compilation

We expect third quarter revenue to be in the range of $1.180 billion to $1.200 billion and third quarter earnings per share to be in the range of $1.30 to $1.36, based on a number of shares diluted and weighted to approximately 175 million shares.

Neil Dougherty, CFO, during Second Quarter 2024 Earnings Call

| Fiscal year 2023 | Fiscal year 2024 | Change in income | |

|---|---|---|---|

| T1 | $1,381 | $1,259 | -8.8% |

| T2 | $1,390 | $1,216 | -12.5% |

| T3 | $1,382 | $1,190 | -13.9% |

| T4 | $1,311 | ? | ? |

Author’s compilation

It should be clarified that this problem is not unique to the company and does not appear to be caused by a loss of market share or competitive advantages. To visualize what I mean, I created this comparison table with companies similar to Keysight but of different sizes.

We quickly see that Keysight is not the only one to encounter problems this year, both in terms of growth and margins. Smaller companies, like Calnex Solutions, have reported a steep 40% decline this year. So, while no one likes their company to decrease revenue by 10%, we can at least consider that this is caused by a general impact on the industry derived from the fact that the customers of these companies (semiconductor companies , telecommunications, among others) ) are also unhappy with the high interest rate environment and are therefore postponing their investment investments.

Author’s compilation

Assessment

Keysight is currently trading at a P/E of 34 using 2024 earnings as a benchmark. That doesn’t sound cheap, but that’s because this year margin compression and revenue declines are expected, as evidenced by the net margin, which fell from 19% in 2023 to 15% in over the last twelve months.

Estimating that there will be a recovery in 2025, which is already starting to be felt in sectors like semiconductors, the P/E would then fall from 34 to 23 thanks to the recovery of profit margins.

In the semiconductor sector, the outlook for the sector is improving with projections for recovery in 2025. Inventories are returning to healthier levels and demand is picking up in some areas like high-bandwidth memory.

CEO Satish Dhanasekaran during Second Quarter 2024 Earnings Call

Market analyzer

I estimate that this year the Free Cash Flow will suffer a greater drop than the turnover this year, but this weak basis of comparison would mean that in the years to come the growth in FCF/Share will be greater than in previous years. , by my estimate, 12% per year, which would be slightly higher than the 10% annual it presented between 2014 and 2023. With this estimate, Keysight would generate almost $12 per share in 2030 and represent a return of 12% in case of purchase at the current price.

Evaluation model (Author’s compilation)

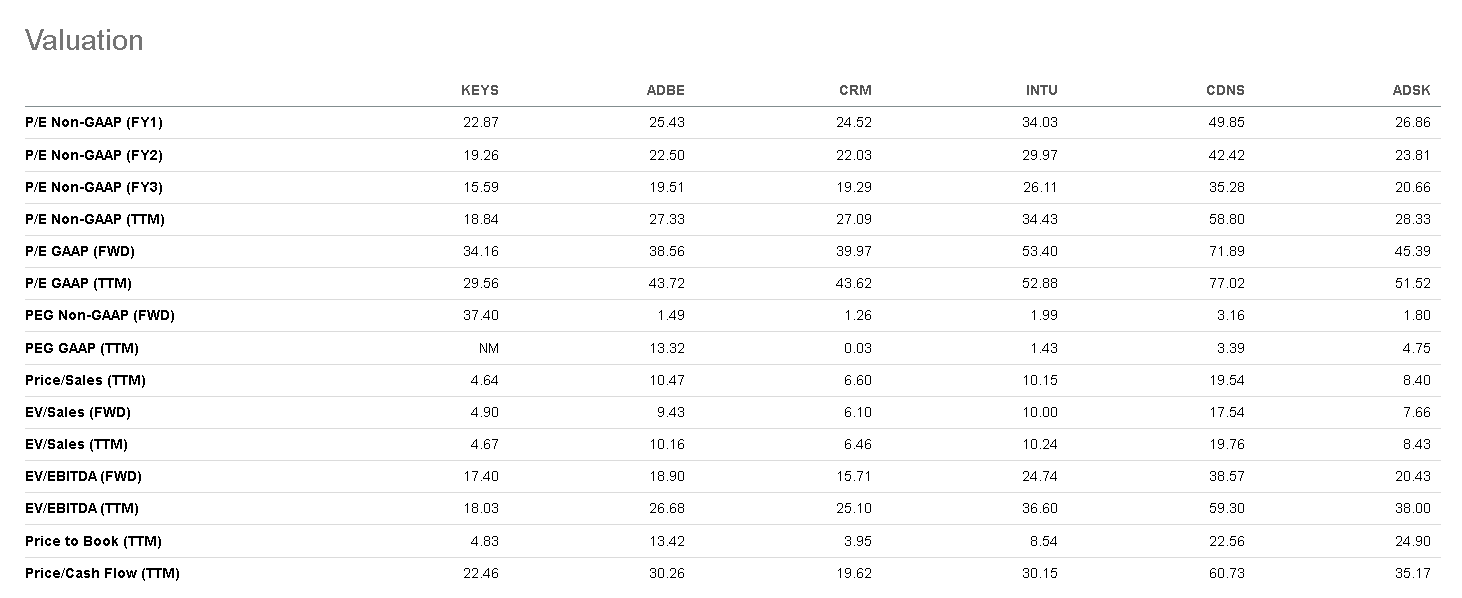

I chose the multiple of 25 times Free Cash Flow based on what we can see from other software publishers. That’s not a very cheap ratio, but it’s hard to find a software company trading at less than 20 times, unless it has structural problems or something that merits a low valuation.

Evaluation ratios (Searching for Alpha)

The essential

As I mentioned in the article, I don’t think Keysight is having any problems that will affect its future. It is not losing market share and the economic slowdown should be temporary, since its services are essential to customers. Therefore, now that the valuation looks better than a few months ago, I am finally interested in buying.

The biggest risk is that the company gains operational leverage, thereby maintaining its costs fixed. This is positive in a growth scenario, but results in profits falling more than revenues in the event of an economic downturn, which may lead to debt issuance to finance itself and could cause my estimate of decline of FCF is lower. In this case, maybe the stock will stay stable longer than expected, but I think if your time horizon is longer than 2 years, then the stock should perform well as an investment.