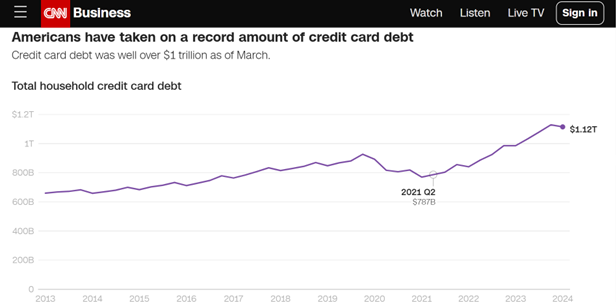

CNN today published an article titled “What is really happening in the American economy”. Most of the points are conventional, but one chart was interesting: credit card debt:

Source: CNN.

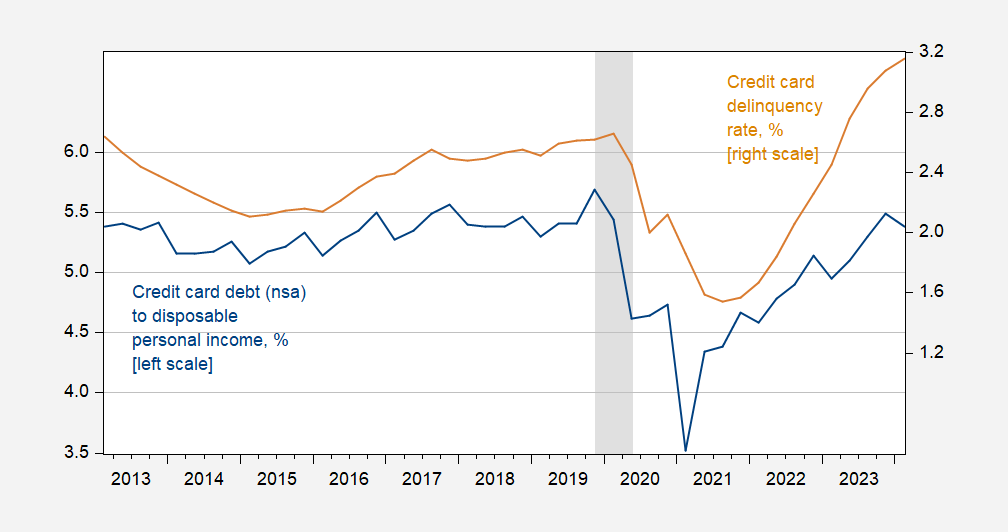

Aside from the usual complaints that this number wasn’t normalized by personal disposable income, or GDP, this struck me as a fun metric to focus on. Here is the normalized credit card debt along with the delinquency rate.

Figure 1: Credit card debt (nosa) to disposable personal income, % (blue, left scale) and credit card delinquency rate for all commercial banks, % (bronze, right scale). The NBER has defined the peak to trough dates of the recession in gray. Source: New York Fed; Federal Reserve Board and BEA via FRED, NBER and author’s calculations.

Thus, normalized credit card debt decreases in the second quarter, but delinquencies increase. This suggests that something is happening for some segments of the population, even as household debt-to-GDP and household debt service-to-disposable income ratios decline.

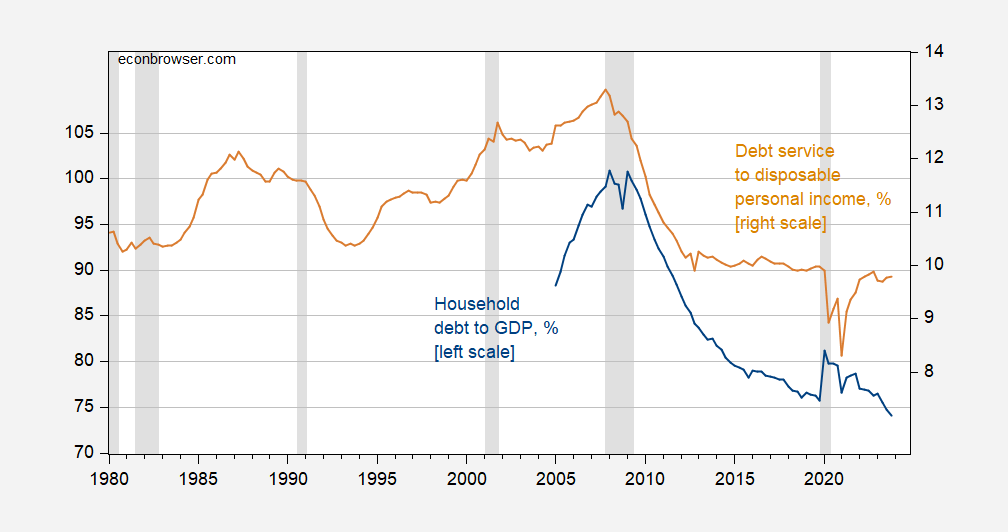

Figure 2: Household debt to GDP, % (blue, left scale) and debt service rate to disposable income, % (beige, right scale). The NBER has defined the peak to trough dates of the recession in gray. Source: IMF via FRED, Federal Reserve Board via FRED, NBER.

Debt service could remain constant even if interest rates rise due to the ubiquity of fixed-rate mortgages. Thus, credit problems are likely more pressing for some income segments than others.