Yes! From Ahmed Rachid and Menzie Chinn, has just published in the Journal of Money, Credit and Banking.

This article has already been discussed in this job; the revised version (August 2023) is here.

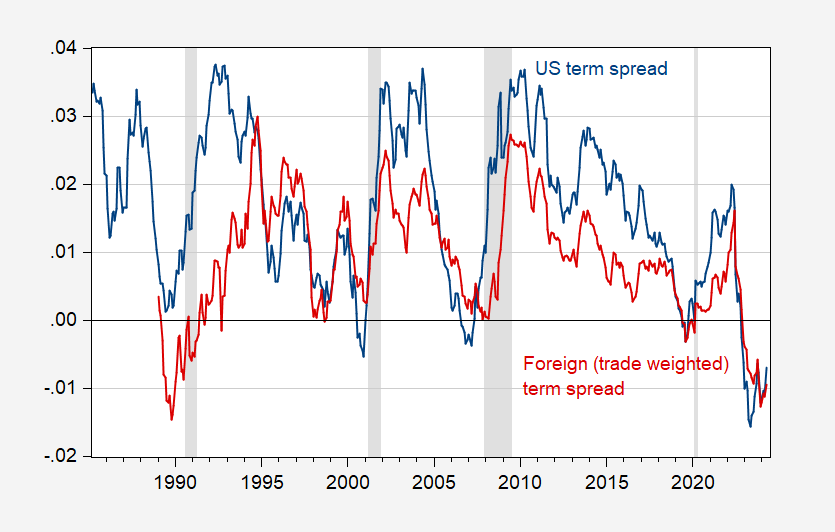

The foreign forward spread (relative to the United States) is shown below. (The foreign spread is the spread weighted by U.S. trade using long-term rates and short-term rates calculated by the Dallas Fed, but in recent years it has been close to the Ahmed-Chinn foreign forward spread used in the document.)

Figure 1: US forward spread at 10 years and 3 months (blue), foreign long term spread at 3 months (red). The NBER has defined the peak to trough dates of the recession in gray. Source: Trésor via FRED, DGEI of the Dallas FedNBER and author’s calculations.