BigBear.ai Holdings, Inc. (NYSE:BBAI), which provides advanced analytics and AI solutions, is overvalued. To make things even more confusing, I believe that over the next twelve months BigBair.ai will be forced to raise money by diluting investors.

Ultimately, I argue that over the next few quarters, investors will view BBAI at $1.76 as a high stock price.

Here I discuss what BigBear.ai does and why I think this stock is a sell.

BigBear.ai is a company that has a very compelling narrative. Indeed, I have to admit that even though I had my doubts about the company, I didn’t put a sell rating on the stock.

Author’s work on BBAI

I recognized that giving a sell rating to an artificial intelligence or AI-based stock, especially a stock with AI on its behalf, it’s not worth it unless I’m completely convinced the stock is going down. In hindsight, it was the right decision to make. But now, as we look ahead to 2024-2025, I think this stock is a sell. Here’s why.

Short-term outlook for BigBear.ai

BigBear.ai specializes in AI-driven business intelligence solutions, serving markets such as global supply chains and logistics, autonomous systems, and cybersecurity.

It is not a lightweight platform, but rather a management consulting service, focused on areas such as cloud engineering. And that will, needless to say, impact the premium at which its shares are expected to trade.

Their solutions enable customers, including federal defense and intelligence agencies, to make informed decisions when processing complex data. Simply put, BigBear.ai’s competitive advantage lies in its team of experts and not its software solutions.

With this in mind, BigBear.ai faces some key and noteworthy challenges. One of the main challenges concerns the impact of contracts like EPASS, which represent existing programs with lower margins.

Additionally, Virgin Orbit’s bankruptcy presents a significant headwind, resulting in lost revenue.

On a positive note, BigBear.ai recognizes these headwinds and strives to achieve positive cash flow while managing non-recurring expenses.

In this context, let’s delve deeper into its fundamentals.

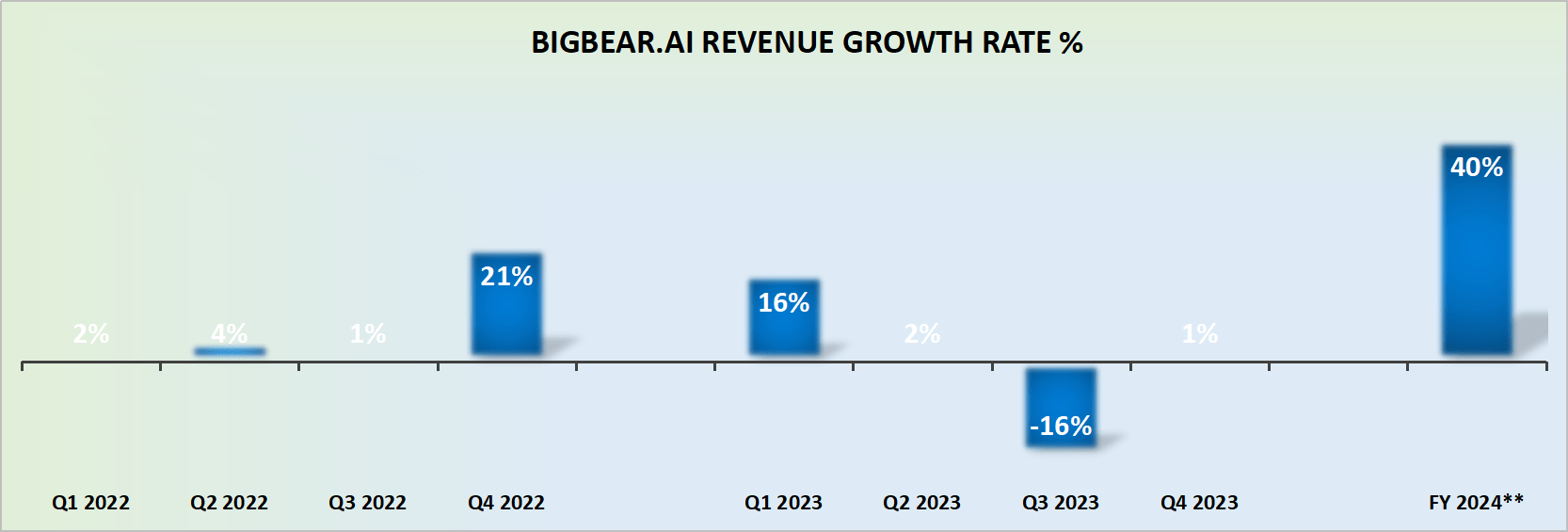

Revenue growth rates are unpredictable

BBAI Revenue Growth Rate

The chart above shows the volatile revenue growth rates that BigBear.ai has generated over the past few quarters. There is a lot to say about BigBear.ai. But what we cannot say is that it is a stable, predictable, recurring and high-growth economic model.

Additionally, to further complicate its growth profile, BigBear.ai acquired Pangiam but failed to determine what its 2024 organic growth rates are likely to be.

Instead, we end up with revenue growth rates showing growth rates of 40%, but little detail as to the underlying drivers of that growth rate.

BBAI Stock Valuation – Overvalued

Review of BigBear.ai holds approximately $160 million in net debt. In other words, more than a third of its market capitalization is made up of its net debt.

Additionally, even though BigBear.ai had positive free cash flow in the third quarter of 2023, that free cash flow was not strong enough to prevent BigBear.ai from having materially negative free cash flow for 2023. More precisely, BigBear.ai burned for a little over a year. $20 million in free cash flow last year.

Even assuming 2024 sees its free cash flow improve slightly, I believe this company is set to raise capital in the next twelve months.

Therefore, BigBear.ai will do everything in its power to put together a strong first quarter (expected May 8), as well as a super polished AI-driven story, so that it can raise additional funds this year, after raising $50 million last year. .

Additionally, BigBear.ai is not a high gross margin software company. Indeed, its gross margins stood at 32.1% in the fourth quarter of 2023, which, while an improvement on the previous year’s 29.2%, is hardly comparable to a purely AI opportunity. This is a low-margin technology company with very unstable growth rates. Avoid this stock.

The essential

As an investor, I recommend avoiding BigBear.ai. The company’s overvaluation is complicated by the high likelihood of fundraising activities over the next 12 months, which will dilute investors.

Additionally, BigBear.ai’s revenue growth rates have been volatile and its acquisition of Pangiam lacks transparency regarding organic growth projections for 2024.

The company’s balance sheet reflects significant net debt, raising concerns about its financial stability. Although BigBear.ai aims to improve its cash flow, its low gross margins and unpredictable growth rates highlight the risks associated with investing in this stock.

Therefore, I am now issuing a Sell rating on BigBear.ai Holdings, Inc. stock.

(NYSE: BBAI)")