")

J. Michael Jones/iStock Editorial via Getty Images

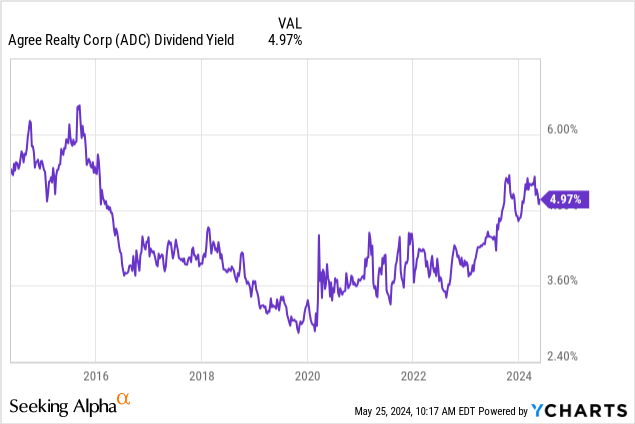

I purchased more products from Agree Realty (NYSE:CDA) common and preferred stocks since the beginning of the year in response to the continued weakness of these securities. Commons are down 9% the last year with the 4.25% series A preferences (NYSE:ADC.PR.A) are trading at a significant 32% discount to their liquidation value of $25 per share. The Commons last declared a monthly cash dividend of $0.250 per share, remained unchanged from the previous month and at $3 per share annualized for a dividend yield of 5.1%. This yield is near a 10-year all-time high, with ADC trading for a 14.4x multiple over the midpoint of its adjusted funds from operations (“AFFO”) guidance for the entire year 2024. $4.10 to $4.13 per share. This multiple was approximately 19x through 2022, just as the Fed was raising base interest rates to a more than two-decade high. Therefore, a decline in rates remains the primary catalyst for positive overall returns for both commons and preferred bonds.

ADC owned 2,161 properties with a total gross leasable area of 44.9 million square feet as of the end of its first quarter of fiscal 2024. This portfolio was 99.6% leased with a weighted average remaining lease term of 8.2 years and with 68.8% of the annualized base rent consisting of investment grade national tenants. Importantly, my investment in ADC is based on AFFO’s growth prospects, growing dividend, and strong balance sheet. The REIT’s forecast to increase AFFO per share by 4.2% year over year at the midpoint will mean the most recent annualized dividend will be covered at 137%, or a payout ratio of approximately 73%. Commons are up with preferences down since I last cover the FPI.

AFFO Growth, Investments and Free Cash Flow

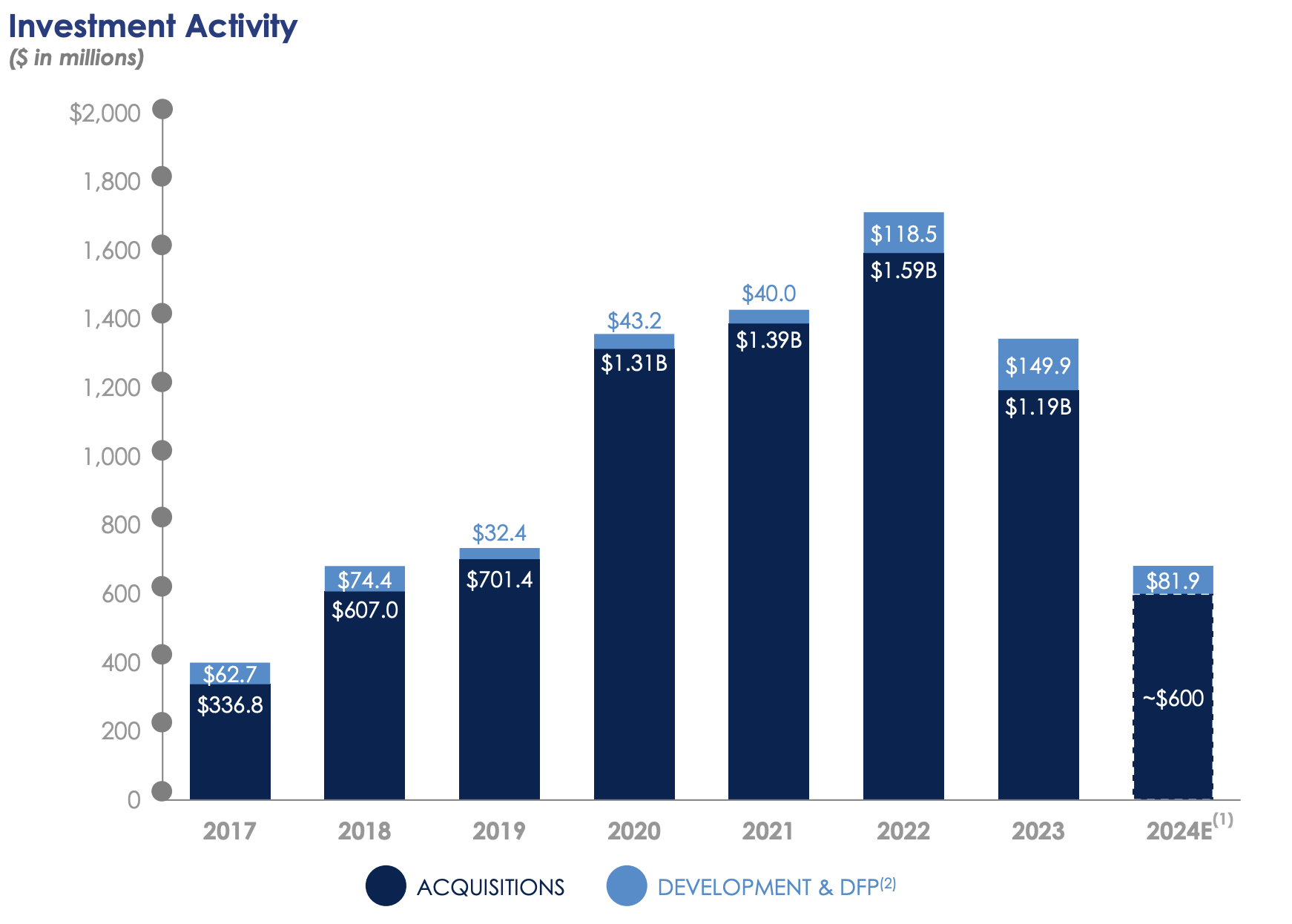

ADC generated revenue of $149.45 million in the first quarter, up 18% from last year and also beating consensus. AFFO per share at $1.03 grew 4.6% year-over-year on continued momentum in net lease REIT investments. ADC invested $140 million in 50 net lease commercial properties during the first quarter, compared to 2024 acquisition volume guidance of 600 million dollars. The REIT also sold six properties for gross proceeds of $22.3 million and at a weighted average capitalization rate of 6.2%. The volume of disposals for the whole year is expected to be between $50 million and $100 million.

Agree Realty First Quarter Fiscal 2024 Presentation

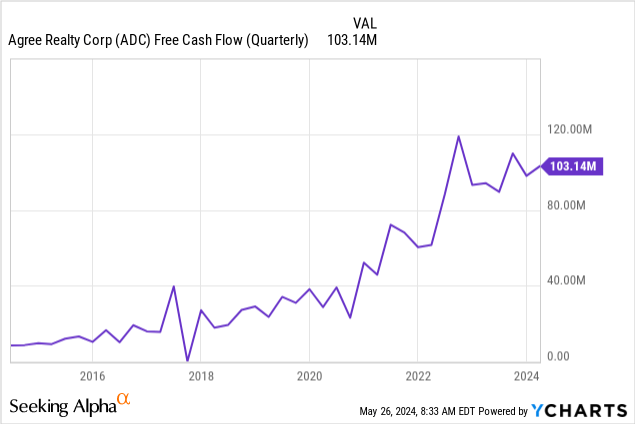

ADC’s weighted average cap rate increased sequentially by 50 basis points to 7.7% during the first quarter, with management targeting investment spreads offering at least 100 basis points over the cost of capital . The REIT’s free cash flow has been growing steadily, providing an internal engine for growth even as acquisitions fall from 2022 highs due to higher base interest rates. AFFO growth combined with the dividend yield implies a near-term total return for ADC of at least 9%, a rate of return that could be boosted if the Fed cuts rates in the second half of the year.

The Prime Opportunity, Debt Maturities, and the Fed

QuantumOnline

ADC preferences provide an asymmetric investment profile. The security was rated “Investment Grade” “Baa2” by Moody’s at the time of issuance in summer 2021. Their annual coupon of $1.0625 has a monthly distribution schedule and, when compared to preferred shares, is trading at 68 cents on the dollar at $17.01 per share. offers a return on cost of 6.2%. These face duration risk, with the discount to liquidation being aware of movements in the federal funds rate, as they were issued at a very low and competitive nominal rate of 4.25%. Recent ADC May 2024 offering of senior unsecured notes due 2034 was finalized at 5.625%, 138 basis points higher than the preferred stock.

Agree Realty First Quarter Fiscal 2024 Presentation

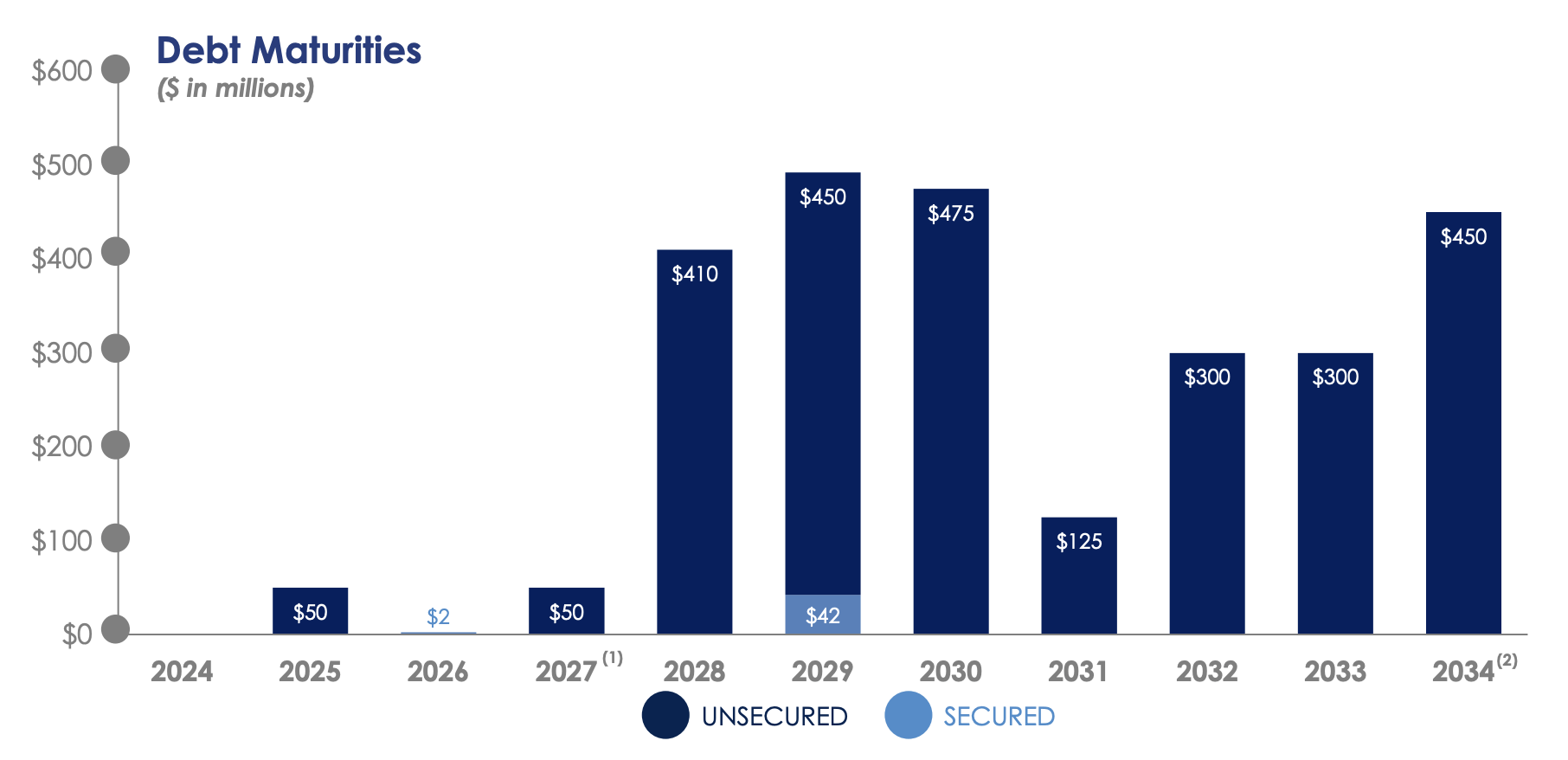

ADC’s debt maturities are also extremely arrears-laden, with only $52 million of debt maturing through the end of 2026. The REIT held total aggregate liquidity of $920 million at the end of the first quarter with $620 million coming from its revolver. The lack of maturing debt means ADC does not face the same refinancing risk as some of its equity REIT peers, giving the REIT the increased ability to pursue acquisition volume and increase AFFOs.

Agree Realty First Quarter Fiscal 2024 Presentation

As a result, ADC offers a near-record dividend yield from a growing portfolio of net lease commercial properties, with preferences trading at a significant discount to their liquidation value despite the safety of the underlying REIT and the Fed’s impending rate cuts. I bought both stocks for strong total return potential, wrapped in the safety of scale and an investment grade rated balance sheet. Short-term returns for both stocks will be mixed and inflation is expected to remain above the Fed’s target, according to the CME FedWatch tool. 25 basis points of cuts as baseline expectations for a 2024 release. I will collect monthly dividends in the meantime.