Philippe Steury

US monetary policy easing is expected to begin later than expected. After a string of stronger-than-expected inflation numbers, S&P Global Market Intelligence analysts now expect the Federal Reserve to make its first rate cut at the December meeting.

Reductions in key rates will not take place until there is “greater confidence that inflation is moving sustainably towards 2%”, according to the Federal Open Market Committee’s statement in may. What this constitutes is uncertain.

This will likely include lower wage growth and the Fed’s target measure, core personal consumption expenditures (PCE) inflation, which is trending around 2%. In line with achieving these goals and in conjunction with weaker US growth, we expect a series of US rate cuts in 2025-2026. A return to the estimated neutral range for the federal funds rate of 2.50% to 2.75% is now expected in mid-2026.

Make the cycles more flexible in As a result, many other economies will start a little later. Expectations of initial policy rate cuts have been pushed back in countries where the currency is pegged to the U.S. dollar, such as Saudi Arabia, or where central banks are battling inflationary pressures and wary of currency depreciation due to the slower pace of Fed easing, such as the UK.

The Bank of Japan is a notable exception. The continued weakness of the yen has led us to bring forward our forecast for the next key rate hike to the fourth quarter of this year, even if the tightening cycle remains rather gradual.

We also continue to expect the European Central Bank to make an initial rate cut of 25 basis points at its next meeting on June 6. The good inflation data and recent communications from the ECB support our view. At the time of writing, futures markets are pricing in an 80% probability of such an outcome occurring.

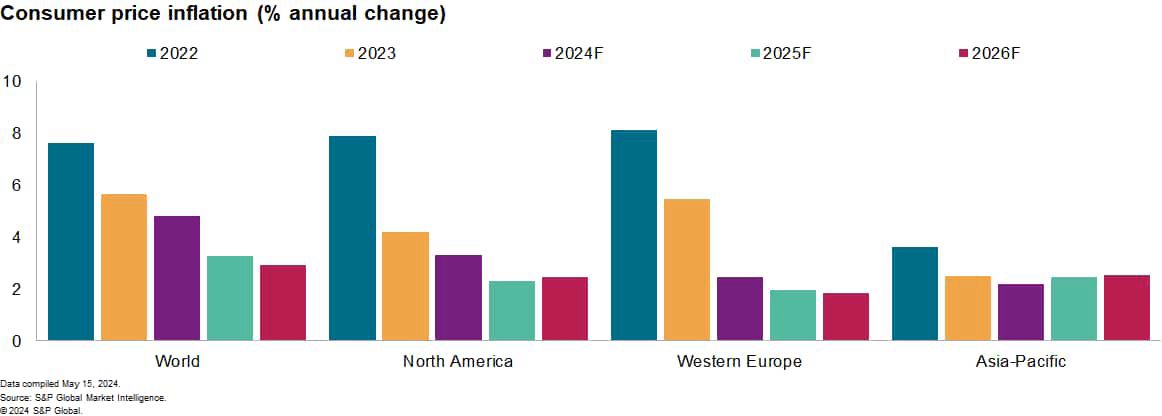

High services inflation rates remain an obstacle to rapid policy easing. Global consumer price inflation fell slightly to 4.5% in March, according to our estimates, just below the 4.7% rate recorded in mid-2023. Although we expect a gradual decline to around 3% by the end of 2025, it will take longer than expected to get there.

A closer look at the components of underlying inflation helps illustrate why. Consumer price inflation for basic goods in the Group of Five economies fell to just 0.3% in March, according to our estimates. This is 8 percentage points below the peak in early 2022.

The equivalent inflation rate for services, which are generally more sensitive to labor costs, reached 4.9% in March. Our forecast for global consumer price inflation in 2024 remained unchanged at 4.8% in our May update, with an upward revision to the US forecast largely offset by weaker forecasts for mainland China and Brasil.

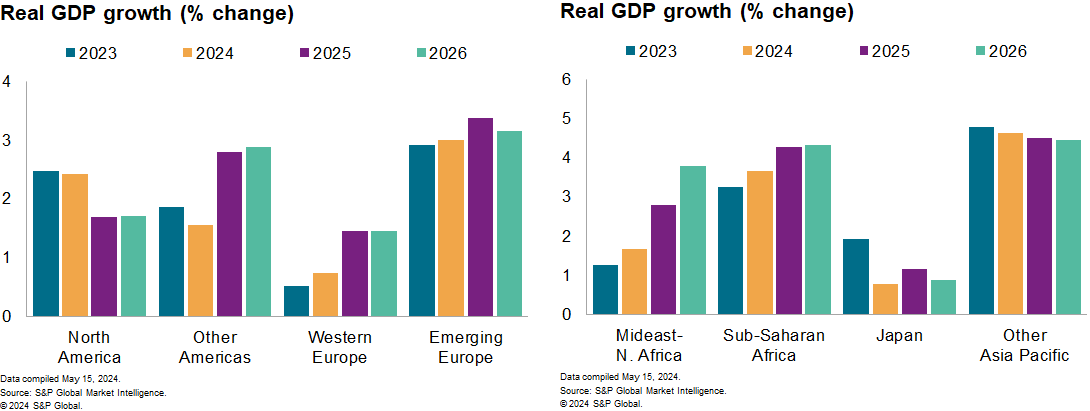

Real GDP growth forecasts for 2024 have been revised upwards in some major economies. These include the Eurozone and the United Kingdom, where early estimates of real GDP growth in the first quarter surprised on the upside.

Relatively moderate growth rates are forecast for the Eurozone and the UK in 2024, at 0.7% and 0.5%, respectively. Growth forecasts for mainland China and Russia also increased slightly in the May forecast series.

As a result, our forecast for global real GDP growth for this year has been raised slightly to 2.7% from 2.6%. The revisions are consistent with improvements in growth momentum reported by data from our Purchasing Managers’ IndexTM (PMI®).

However, a variety of headwinds are expected to prevent global growth rates from reaching the peaks typical of previous expansions, including financial conditions that will be somewhat less accommodative than expected and geopolitical uncertainties.

The recovery in global PMI data appears to be stabilizing. Although the composite index of world production improved for the sixth consecutive month in April, increases over the past three months have been modest. At 52.4, the April level remains below its long-term average (53.2).

The gap between the composite production indices of emerging economies (53.6) and advanced economies (51.8) narrowed to a six-month low in April, helped by the recovery of economies in Western Europe.

The global manufacturing production index was just above the expansion level in April (50.3), although the export orders subindex continued its upward trend, once again indicating plus a recovery in world trade. Supplier delivery times continued to shorten, confirming the limited effects of shipping disruptions.

Editor’s note: The summary bullet points in this article were chosen by the Seeking Alpha editors.