Industrial production at +0.6% m/m vs. +0.3% consensus (manufacturing production +0.4 vs. +0.2% consensus).

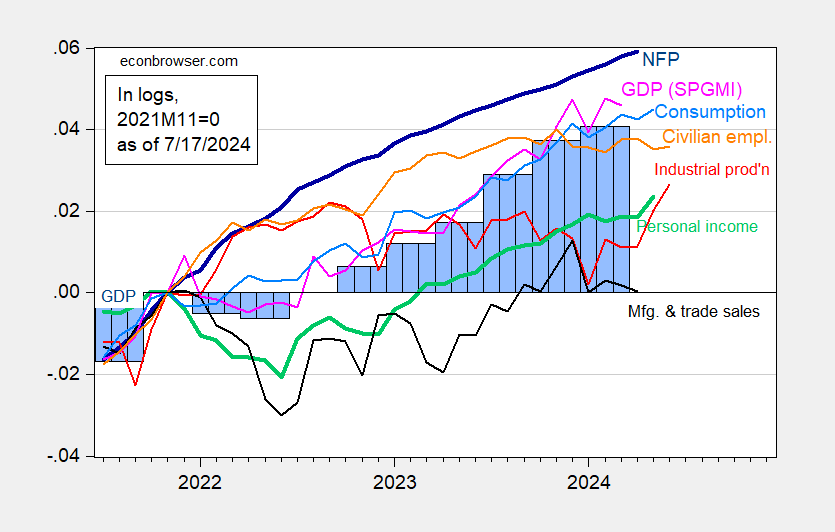

Figure 1: CES Nonfarm Employment (NFP) (bold blue), civilian employment (orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue) and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log-normalized to 2021M11=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q1 Third Release, S&P Global Markets Insights (formerly Macroeconomic Advisors, IHS Markit) (7/1/(version 2024) and author’s calculations.

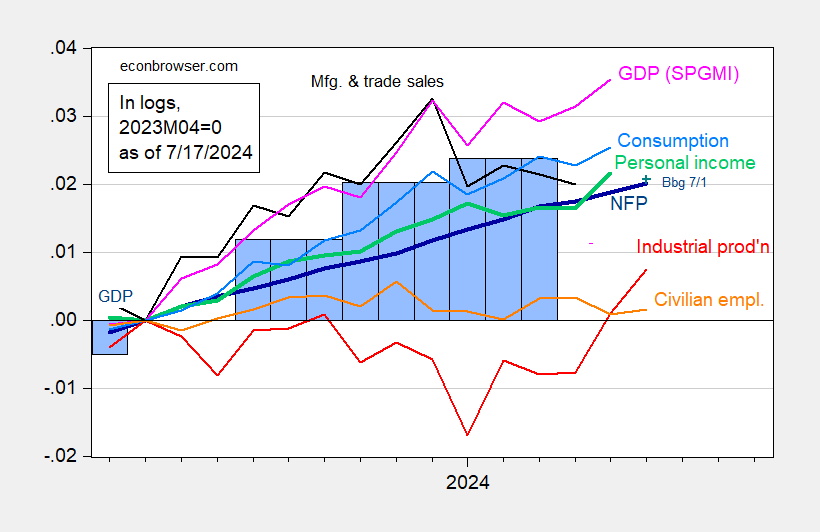

Normalized to April 2023:

Figure 1: CES Nonfarm Employment (NFP) (bold blue), civilian employment (orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue) and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log-normalized to 2023M04=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q1 Third Release, S&P Global Markets Insights (née Macroeconomic Advisers, IHS Markit) (7/1/(version 2024) and author’s calculations.

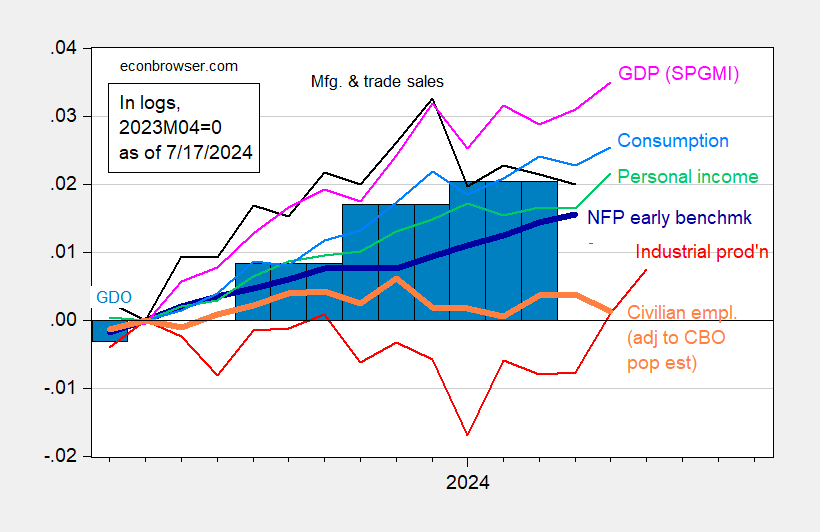

Alternative indicators for production and employment:

Figure 3: Nonfarm Payrolls (NFP): Philadelphia Fed Early Benchmark (dark blue bold), CBO Immigration-Adjusted Civilian Employment (orange), Industrial Production (red), Personal Income excluding Current Transfers in Ch.2017$ (green bold), Manufacturing and Business Sales in Ch.2017$ (black), Consumption in Ch.2017$ (light blue) and Monthly GDP in Ch.2017$ (pink), GDO (blue bars), all log-normalized to 2023M04=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q1 Third Release, S&P Global Markets Insights (née Macroeconomic Advisers, IHS Markit) (7/1/(version 2024) and author’s calculations.

GDP is now revised upwards to 2.7% in the second quarter.